The Exploitation of Retail Investors

Looking at the issues resulting from payment for order flow, maker-taker rebate models, regulation nms, and the lack of hesitation from Wall St. in screwing over as many people as possible.

Investors are either not aware or they do not care. But they will.

“The mighty edifice that is Wall Street was not built on the fortunes of flamboyant speculators, as myth would have it – it was built on pennies.”

Excerpt From: John Coates. “The Hour Between Dog and Wolf.”

Exploiting Retail Investors as a Standard Practice

When John Q Public and Jane C Investor finally realize that they have been getting nickeled and dimed (literally) for over 10 years by the same people who claimed to have their best interests in mind is going to result in a controversy of epic proportions. The public disdain for the financial services industry that is still lingering from the financial crisis of 2007/2008 and subsequent tax payer bailout will only add fuel to this potential fire. Unfortunately, the timing of these events actually unfolding is most likely going to be during, or just slightly before, the next major market crash.

Something needs to be done to prevent these issues from evolving into another major crisis. The only investors and traders left in the aftermath will be the brokerages themselves, and of course the predatory algorithms that have spent much of the previous decade ripping off the people represent the most important resource that exist in the market. The loss of investor confidence leading to their discontinued participation in the market is the primary issue that must be addressed and managed. Instilling confidence in retail investors is hardly possible without managing the issues that are causing them to lose confidence in the first place. The rules established by the creation of Reg. NMS are an excellent starting point, and an analysis of the subsequent effects of these rules from the perspective of retail investors will provide a solid foundation for an issues management framework.

PAYMENT FOR ORDER FLOW (PFOF)

Payment for order flow is exactly what it sounds like: the purchase or sale of orders for marketable securities (stocks, ETFs, options, etc.). PFOF can be broken down into two distinct subcategories: maker-taker rebate models and internalization of retail order flow by broker dealers.

MAKER-TAKER REBATE MODELS

Stock exchanges increase their profits as they receive more orders routed to trade on their exchange. Many exchanges offer incentives to broker dealers for routing their customers’ orders to their trading venue. These incentives are often in the form of a small kickback or rebate that is paid per share. From the perspective of the broker dealers, this can be very attractive considering that typically routing orders involves paying a small fee per share.

An order routed to an exchange for execution will have 2 effects. It will either remove liquidity executing against an order already on the book at that exchange, taking liquidity. Otherwise the order will rest on the book, making liquidity, until such time that another order arrives and a trade can occur. Some exchanges provide rebates for taking liquidity while others provide rebates for making liquidity. The same applies for fees charged. This maker-taker system creates a situation where routing an order that is currently marketable, meaning a market order or a limit order that is above the lowest offer, in effect making it a market order, will result in either a fee or a rebate depending on where it is routed. Now imagine you are a broker dealer deciding where to route some client orders that you just received. This decision made by computers anymore but for the sake of argument let’s just pretend it isn’t. Are you going to choose to route the orders to an exchange that incurs a fee or one that provides a rebate? Even those vehemently in favor of this maker-taker payment model will admit that conflicts of interest are possible.

The fact that the main architect of PFOF was none other than Bernie Madoff should immediately lead one to assume that it might have uses in the exploitation of market participants. Fortunately, we have the SEC to protect investors from regulations that might be used in malicious ways. Given that their stance on PFOF can be summarized from their comment on the matter: “The competition for order flow among these venues is intense and it benefits investors by encouraging services that meet particular trading needs and by keeping trading fees low”. Sure, competition is a positive thing to have in a market and prices will be lower but why is there so much competition over orders submitted by retail investors?

Professional Traders and broker-dealers willingly pay to purchase retail order flow for two reasons: risk reduction and exploitation. Generally, retail orders are purchased ahead of the publicly displayed price quotations with the knowledge of what these immediate price quotes will soon be. This is why the order flow from retail investors is in high demand: since it can be determined whether or not a profit can be made before even having purchased the order flow. Critics of the PFOF model have made the argument that it can almost be considered a form of insider trading since the people purchasing the order flow have advanced and privileged knowledge of the competitors, or that is to say other investors/traders. Insider trading is defined as using non-public information for gaining an advantage ahead of an event that is defined by a release of information that was not otherwise known to the general public previously. Arguments on both sides do have validity since payment for order flow has been shown to increase liquidity and provide “price improvement”. But if the intention of Regulators is to provide a framework that establishes a fair and orderly market while creating an equal opportunity for all participants, then they have utterly failed.

INTERNALIZATION

The other subcategory of PFOF is order flow internalization. What this means is broker-dealers execute their customers’ orders against one another or against purchased order flow from other brokers all within their own internal trading venue or via a wholesaler. A customer's trade is executed without the order ever being routed to a stock exchange such as the Nasdaq or NYSE. Retail investors are extremely limited in their ability to route their orders to specific venues. Their broker routes customer orders to one of the numerous wholesalers (also known as internalizers or market makers) with whom the broker has a PFOF relationship. This benefits the broker since most wholesalers generally provide a rebate for order volume regardless of the effect on liquidity.

This has been the standard operating procedure for almost a decade. The reason being that routing orders in this manner does in fact provide investors with a minute amount of price improvement on their executions. This price improvement constitutes the backbone of the argument for PFOF and has certainly helped keep complaints from investors at a minimum. But what neither the brokerage firms or the wholesalers want anyone to know is that a price improvement of 10 cents to the retail investor translates to $4.90 in profit for the wholesaler and $2.00 in profit for the broker. That is for a market order. For limit, orders the distribution becomes $13.33 for the wholesaler, $4.00 for the retail broker, and (drum-roll please) $0.03 of price improvement for the retail investor. Retail investors do get a bit of a boost in price improvement with stop orders where in one example they receive $2.00 dollars of price improvement while the wholesaler only receives $43.00 and retail broker $4.00. Given this information, retail investors should not be happy about this pathetic price improvement they receive when it is really only intended to keep them happy enough not to look into the matter further and discover who the true benefactor of the price improvement transaction really was.

Regulation NMS (National Market System)

Regulation NMS was created in 2005 before the financial crises that would follow in the few years that followed. The goal of this regulation was to provide additional transparency, promote competition between individual markets (NYSE, NASDAQ, etc.) and level the playing field between retail investors. Two of the major components of Reg NMS are the sub-penny rule and the order protection rule. Reg NMS admittedly does seem like a positive piece of legislation on the surface but sadly it has ultimately become one of the most disadvantageous forces for retail investors ever conceived. Not only was the market not made more fair for all participants but it actually provided the tools needed to exploit retail investors even further.

ORDER PROTECTION RULE

Reg NMS requires that orders must be executed at the best possible price available in the market at the time the order is received. Nothing wrong with that right? Well, first of all, the list of exceptions or reasons for which this rule need not be adhered to is nearly 3 times as long as the actual rule itself. The other caveat is this “best possible price” notion. Prices can change very fast and prices for the same securities are listed on every exchange where that security is traded. In a perfect world, when the price of a stock changed on one exchange it would simultaneously change on all the others. Obviously, this is not the case and it takes time for this information to travel.

To solve this issue of needing to execute an order at the best possible price Reg NMS established the NBBO. This is an acronym for the “national best bid and offer” which is distributed to all exchanges from the Securities Information Processor or SIP. The SIP aggregates the top-of-the-book bid and offer (ie the bid/ask you would see on yahoo finance for example) from each exchange and then distributes that information to all the exchanges. Doesn’t seem like an unreasonable way of ensuring all the exchanges executing orders are using the same ‘best’ price for executions. There are just two slight problems that occur when this practice is implemented in the real world

First, the distance between exchanges and the SIP varies for each exchange. This means that the NBBO dissemination requires data to be sent from all exchanges, which is then aggregated at the SIP, after which the information is redistributed back to the exchanges. This all occurs in a matter of milliseconds and the signal from the SIP is not received at exactly the same time by every exchange. As you might expect, these exchanges have received additional orders in the time it took to receive the updated NBBO. This is why the ‘best possible price’ at which an order is executed may in reality not truly be the best price available if the NBBO at that exchange is “stale”.

The SIP, until just recently, was a slow (say Windows 98) piece of hardware. The exchanges themselves all have direct feeds to each other in order to receive and send market data which they in turn use to calculate a more real-time NBBO. The feeds are several milliseconds faster than the SIP and although orders must be executed at the best price, knowing what the best price will be, even only less than a second from now, is extremely valuable. Especially when Reg NMS gives priority to orders that are marketable at the time they are received to be executed at the NBBO prices. The bottom line is that even though the exchange or broker dealer may have the knowledge that the best price is “stale” they are still within the rules when executing the order at the stale price. In fact, they can even be penalized if they don’t.

SUB-PENNY PRICING

Another major component of Reg NMS is the sub-penny pricing rule. Sub-penny pricing is used extensively in the exploitation of retail investors and is what makes the predatory practices of PFOF possible. If you are still on the fence as to whether Reg NMS benefits retail investors, then perhaps this will help you decide. This regulation which was meant to create fair and orderly markets with equal opportunity for all participants allows only certain market participants to use the sub-penny rule while everyone else is not allowed. Coincidentally, it is the sub-penny rule that allows brokers and wholesalers to trade inside the spread and maximize the benefits of PFOF while effectively screwing all of the regular people in the process.

Here is how sub-penny pricing is disadvantageous provides price improvement to retail investors: Suppose you submit a market order to buy 1000 shares of stock X, which is currently trading at $39.99/$40.00 (bid/ask). Your order is routed to wholesaler who knows that the market for Stock X is, or will be within a few milliseconds, is $39.98/$39.99. The wholesaler, internally, sells you short 1000 shares at $39.9999/share giving you a price improvement of 10 cents. Almost instantaneously as the updated NBBO arrives and the price updates the wholesaler buys 1000 shares to cover the short at $39.99 representing a $9.90 profit for the wholesaler. Internalization. Brought to you in part by Reg NMS.

Since the customer got a better price it is hard to make a case that this practice is harmful. But what if the outcome had been different if there was no 3rd party involved in trade? That is what is lost and what customers are being robbed of; a non-quantifiable alternate possibility. Retail investors placing orders to buy and sell are putting their capital at risk by adding liquidity to a market which ultimately repays them by exploiting them to the fullest extent possible within the constraints of the law. Compliance with the law was never meant to mean compliance with morality.

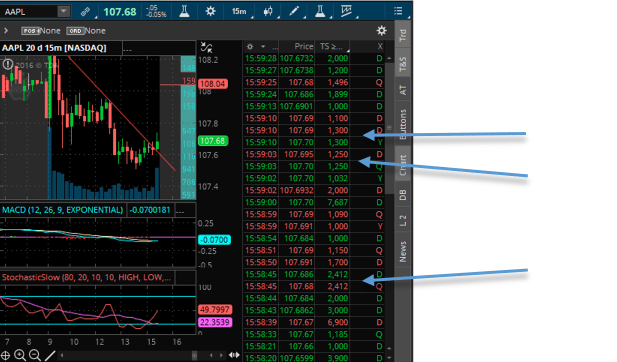

Arrows pointing to possible “price improvements”. Notice the share quantity in column 3 and the different prices in column 2.

Can you spot any price improvement? Or any trades that were made NOT in sub-penny increments?

The Basis for Not Caring

A major reason that many of these issues are still not fully realized is the lack of public outcry over these various practices of exploitation. Since most retail investors are not even aware that any of this is happening, or if they are aware and happen to be benefiting, if by only fractions of a penny, they just don't care.

Although the general public might not be as concerned about all of this malpractice and getting jipped out of a couple of fractional pennies on their trades, there is one group of people does who care immensely: professional money managers. The people running mutual funds, hedge funds and pension funds, which have large turnover in assets, meaning they are buying and selling large quantities of shares care a great deal. Fractional pennies don’t mean that much on 100 shares of stock but on a million shares of stock, it is going to affect that money managers bottom line.

So, What’s The Issue?

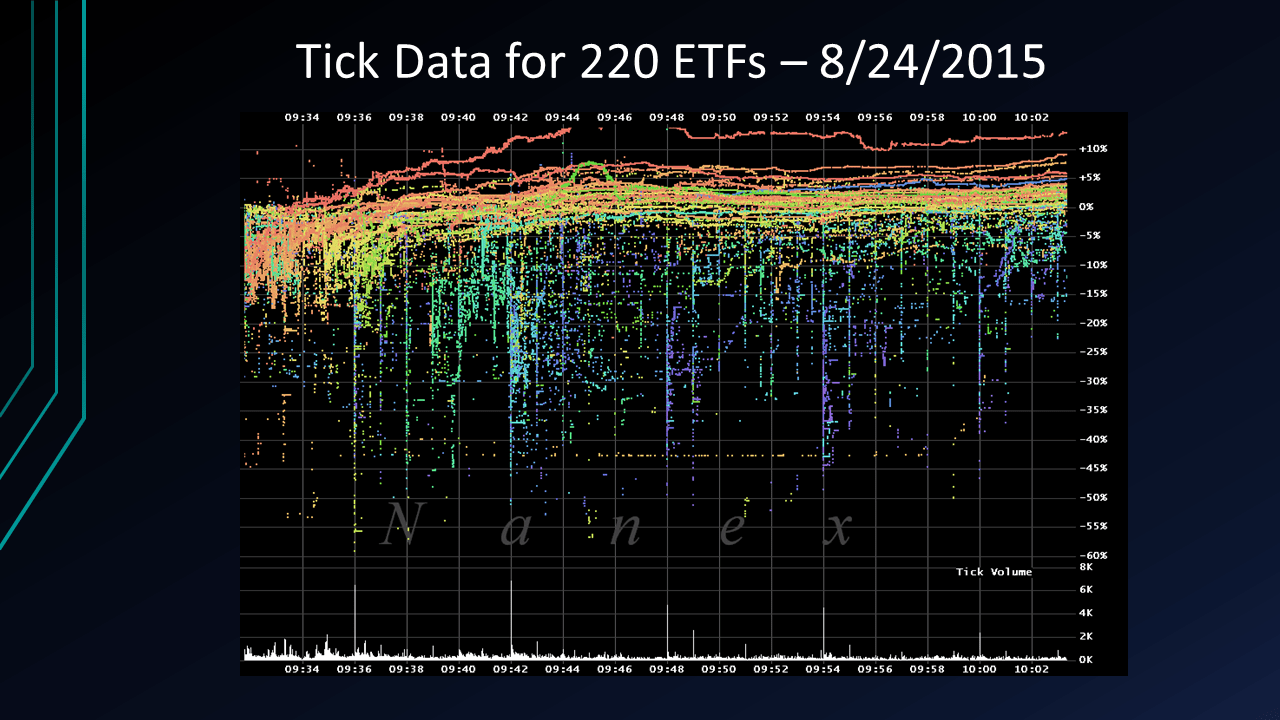

To be perfectly clear what I have discussed thus far is technically the standard practice anymore. The problem however, and where the issues arise from, is the degradation of the markets to the extent that retail investors no longer have any interest in participating because they no longer feel it to be fair. As this trend continues the market loses liquidity which in turn further perpetuates the trend. There will always be passive investment ETFs, retirement funds, and things of that nature but without liquidity in the market they will no longer be safe investments. Your retirement account might be up a good percentage but if there is no one in the market willing to buy your shares from you then you could be in a tight spot. Without liquidity bad things can happen. Take August 24th, 2015, for example. Stop-loss orders for various ETFs were executed at prices well below the fair value of the ETFs because liquidity had evaporated. All of the machines turned off and all of the sell orders that executed in that couple of seconds yielded the sellers massive losses. If you were an investor that had been informed your 25K holding of an ETF had been sold for a 40% loss at a price that existed for a mere couple of microseconds I doubt you’d be happy about it. The next day when you read that 8/24 was the most profitable day ever recorded for a particular wholesaler/market-maker (this is a true story) you would probably just start keeping your savings under the mattress.

Each color represents a unique ETF and each dot a unique trade.

Source: Nanex LLC

Market volumes are abysmally low in the present time. Whether it is because of the seasonal aspect or whether people are frustrated and no longer participating who knows. But when an ETF that generally trades over 100 million shares a day on average is currently averaging about 25 million shares in volume over a day, you had better bet that the machines and algorithms designed to exploit the situation are having a field day while the retail investors are cursing at their computers.

Effectively Managing/Preventing Furtherance of These Issues

Investor confidence, or lack thereof, as well as the degree to which retail investors are disadvantaged almost as much as they are exploited is the overarching theme of all of these underlying issues. Together these issues will lead to retail investors exiting the market further perpetuating the problems. This trend is continuing and in conjunction with a market crash or major market correction would certainly spell trouble for financial markets.

There are several approaches by which these issues can best be managed before they become a crisis. Given that the current regulators and lawmaking bodies are much of the reason any of this has been able to come to pass means that simply changing the rules probably won't work or won’t be possible. Ignoring that fact, the ideal approach would start with first eliminating the sub-penny pricing rule and create a rule that prevents order from being internally executed but instead requiring them to actually be routed to a stock exchange.

A more plausible management strategy is educating retail investors on how they are being exploited and the steps they can take to avoid such exploitation might just be the best management strategy for the issues discussed. Not only would this allow retail investors to avoid some of these insidious practices should they care about them or have desire to avoid them, but will prepare them for the worst-case scenario which is not too far down the road.

The more retail investors that become educated as to the under workings of the financial markets and some of the things that are wrong with it the better chance there is to actually change the rules. Also, if people knew full well what is happening behind the scenes and how they are getting nickeled and dimed but still choose to carry on anyway then at least there would be no need for sympathy.

The old saying “he who has the gold makes the rules” is relevant in this context. High frequency trading firms and broker-dealers that bring in lavish profits year after year are the biggest proponents of keeping things the way they are. But for that to happen, retail investors need to continue participating in the markets. Otherwise these firms will no longer have any retail investors to exploit.

Food for Thought

For the finale, I leave you with a quote regarding revenue generated by an exchange:

"BATS earns additional revenue by charging those HFT firms that want to know about investor orders on EDGX for the EDGX Depth Attributed proprietary market data feed that identifies those retail investor orders. That feed allows HFT to know about the presence of retail investor orders at each price level on EDGX and the relative queue priority of retail investor orders at each price level. HFT’s that consume that EDGX Depth Attributed feed and the direct feeds from all other exchanges can then identify situations where they know the stock is about to move in favor of the clearly marked retail investor and execute against that retail investor order just before the investor might have otherwise bought the stock for less (or sold it for more). The HFT can then immediately buy/sell their resulting position for a quick risk-free profit."

An animation showing exactly how the frontrunning that occurs to facilitate profiting from internalization: https://www.youtube.com/watch?v=f9EjJoCNtoo

I tried to avoid getting to detailed about the process by which brokers and wholesaler profit from the spread of retail investor orders but I encourage you to take a look at a fantastic short read (written for the layperson) that explains in detail how various order types are processed as well as how the above mentioned numbers are made possible.

Example Rule 606 Disclosures showing how and to whom orders are routed.

https://www.tdameritrade.com/retail-en_us/resources/pdf/AMTD2055.pdf

https://d2ue93q3u507c2.cloudfront.net/assets/robinhood/legal/RHF PFO Disclosure.pdf